I would have similar comments here as those as I had for TLO in terms of just letting them drill out the Dumbwa mega-target. MMA has 5 rigs running and loads of cash on hand, so my plan is not to react to any individual batch of drill results.

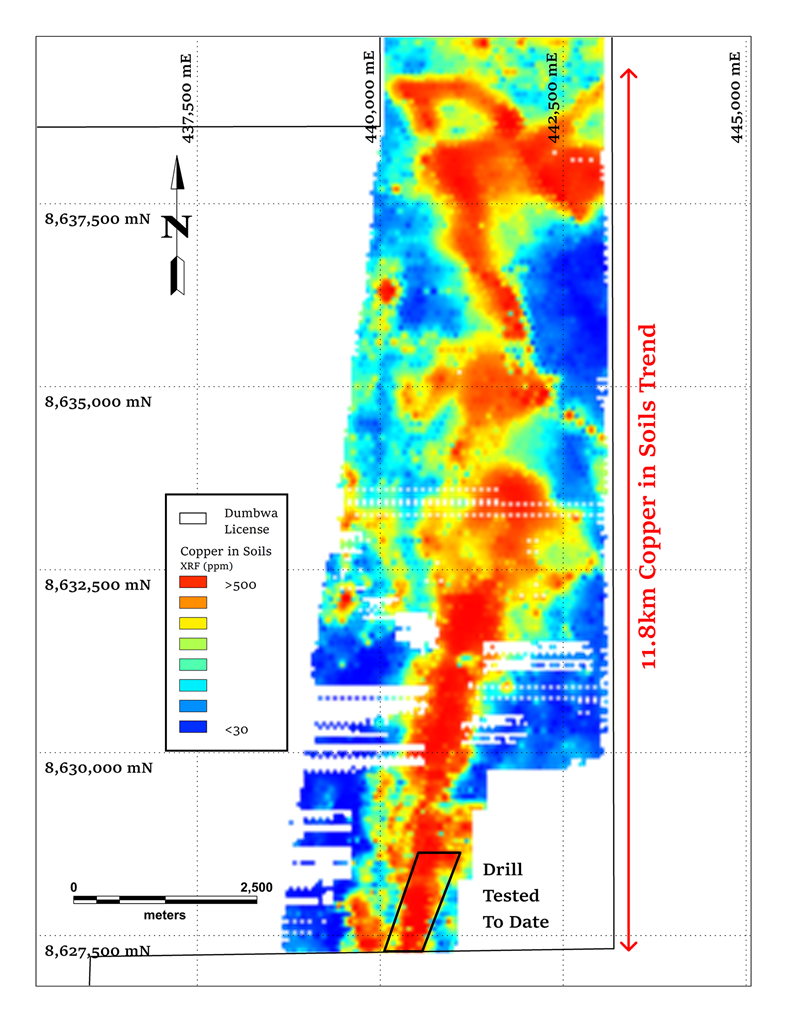

There is potentially 11 kilometres of strike length in play in a corridor that may be on the order of 300 metres wide. This is a massive copper trend. What may be most interesting is the excellent correlation that the company sees between surface soil geochemistry (copper in soils) and the underlying mineralization. MMA is methodically drilling out a huge, near vertically oriented, mineralized shear-zone corridor that contains multiple mineralized parallel shear zones within it.

As a whole, the corridor may be some 300 metres wide — perhaps wider in parts and narrower in others. Mineralized shear zones near the core of the trend typically exhibit higher grades and contain copper-bearing sulphide minerals like bornite, cuprite, and chalcocite, while the shears further from the core are chalcopyrite-dominant. Reducing it to its most basic form, think of it as a meandering river of copper-mineralized material.

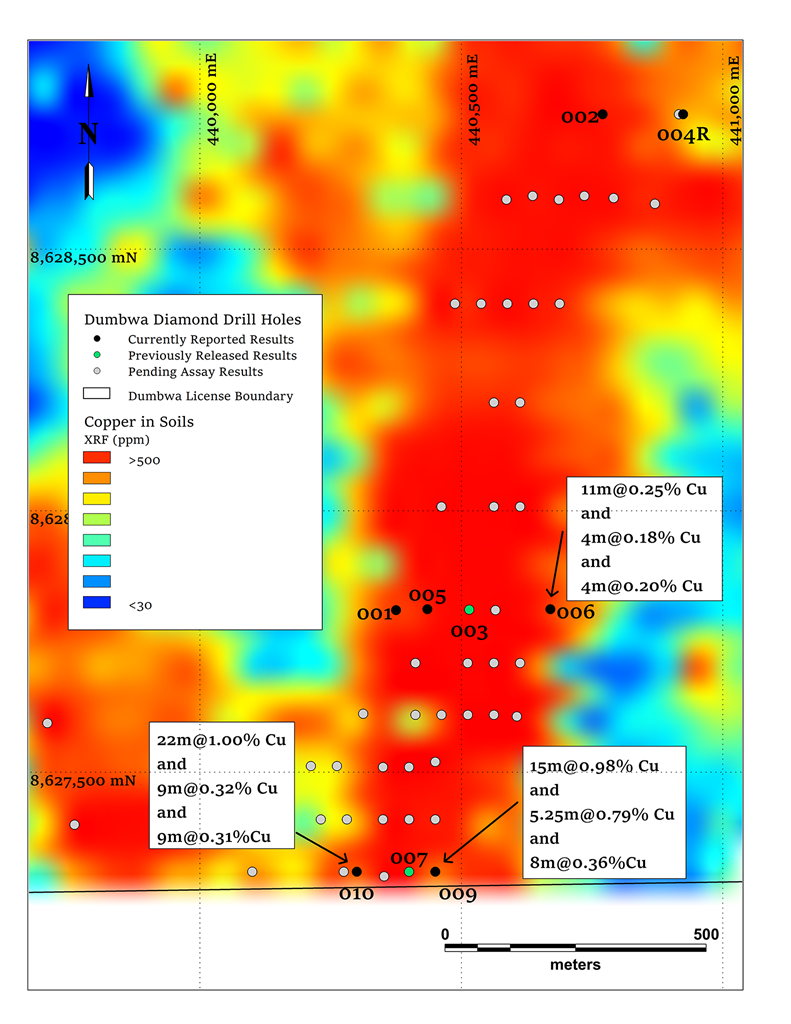

MMA hosted an investor call on Wednesday to run through what they're seeing thus far, and probably the key takeaways for me were that: 1) mineralization at Dumbwa is very predictable, and 2) the mineralization starts just 3 metres below a thin soil cover. This explains the good correlation they are seeing between mineralized intercepts and soil geochemistry.

It also has significant implications for just how low-cost mining this deposit could be. A mine here would look like a big channel cut perhaps only 200-300m deep, with steep walls and a very low strip ratio (i.e., you're just scraping off a veneer of dirt, and then mining out the top 200-300m of the "river" of mineralized material within the shear corridor). With a strip ratio this low, even a bulk grade 0.2% Cu would be economic – and MMA thinks the bulk grade could be 0.3-0.5%.

There will be hotter areas and less hot areas, but overall I believe that a coherent bulk tonnage target will emerge here. The company laid out potential tonnage scenarios and every one of them was impressive – with some approaching 2 billion tonnes. In due course, I think this will attract interest from the real miners out there.

They have drilled 88 holes thus far and will be up to 6 rigs in January. The assay labs are backed up – as MMA is making sure that the results they are getting are accurate through a thorough quality control protocol – but visual mineralization is consistent and predictable. It's important to remember that only a handful of holes have been released, but with this kind of deposit, visually, the company can already see what is unfolding at Dumbwa, which is what makes MMA so interesting to me.

The correlation between drilling intercepts and the copper-in-soil anomaly means that MMA has a somewhat mechanical task of just drilling out an absolutely massive trend. Based on what we know today, this trend isn't going to be hard to follow… and in mining predictability is good.

So when will the market really take notice? Hard to say. It seems unimpressed, but I think that the reality of Dumbwa still requires a leap of faith for some, but I don't think it's a huge leap. All you have to do is listen to what the copper-in-soil anomaly is saying in conjunction with the visuals in the drill core.

The model makes sense… a large-scale shear zone with mineralization that is zoned across its width. Eventually, I think the company will cut a deal with First Quantum for the oxides at Kazhiba and that will be the day that a whole new raft of investors will discover MMA for the first time. Meanwhile, Dumbwa has all the ingredients needed to be a monster deposit – so time (i.e., drilling) will tell.

My takeaway is that there is nothing to do but wait and let them drill it out. Tick tock.

LIBRARY · APR 2026 · $1.30

LIBRARY · APR 2026 · $1.30